How to Create Your NAPSA iCare Profile: A Complete Step-by-Step Guide

A practical walkthrough of NAPSA iCare registration in Zambia — what documents you need, how the process works from start to approval, and how to estimate your monthly contributions in Zambian Kwacha (ZMW).

Updated for 2026 · Estimated reading time: 9 minutes

Why a NAPSA iCare Profile Matters

The National Pension Scheme Authority (NAPSA) is Zambia’s mandatory social security scheme, covering virtually every employed person in the formal sector. The iCare portal is NAPSA’s digital self-service platform, giving members and employers a single place to register, update personal details, view contribution history, submit returns, and manage payments without visiting a branch office.

Whether you are a new employee setting up your account for the first time, an employer onboarding staff, or a Zambian working abroad who wants to keep contributing toward retirement benefits, the iCare profile is the foundation for almost everything else you’ll do with NAPSA. Getting it right the first time — with the correct details and properly formatted documents — avoids delays that can hold up access to benefits, loan applications that require NAPSA statements, or employer registration down the line.

This guide walks through the registration process from start to finish, flags the most common reasons applications get rejected, and includes a contribution calculator so you can estimate what you (or your employer) should be paying each month, in Zambian Kwacha.

What You’ll Need Before You Start

Having the right documents ready before you open the registration portal will save you from stopping halfway through a session — something that can cause timeouts and force you to start over. Make sure you have:

- National Registration Card (NRC): Clear, color copies of both the front and the back. Black-and-white scans or photos with glare are a common cause of rejection.

- Passport photo: A recent photo taken within the last six months, with a plain background and no sunglasses or hats.

- Active mobile phone: The SIM must be registered in your own name with your network operator, since this number is used for OTP (one-time password) verification.

- Valid email address: Must be unique — that is, not previously used to register a different NAPSA account.

It also helps to know your full legal name exactly as it appears on your NRC, your date of birth, and your current residential address, since these fields are checked against your uploaded documents.

Step-by-Step Registration Process

Access the Registration Portal

Go to the official NAPSA iCare website at icare.napsa.co.zm. On the homepage, click the “Register” button, then select “Create New Account” to begin the registration process. Avoid third-party sites that claim to offer NAPSA registration — always use the official portal address.

Choose Your User Category

NAPSA splits applicants into four categories, and choosing the right one determines which fields and document requirements you’ll see next:

- Zambian citizens in Zambia — the standard registration process for most employed Zambians.

- Zambian citizens abroad — a modified process for diaspora members who want to continue contributing or manage existing benefits remotely.

- Foreign nationals in Zambia — for non-Zambians working in the country under NAPSA-covered employment.

- Foreign nationals abroad — for non-Zambians working outside Zambia who still have a NAPSA-linked employment arrangement.

Complete Your Personal Information

Enter your full name exactly as it appears on your NRC, your date of birth, NRC number, gender, and nationality, followed by your current address details. Small mismatches — such as a missing middle name or a different spelling — between this form and your uploaded NRC are one of the most common reasons applications are sent back for correction.

Upload Required Documents

Upload clear copies of your NRC (front and back) and a recent passport photo. Documents must be in PDF, PNG, or JPG format, and each file must not exceed 5MB. Before uploading, double-check that:

- All text on the documents is sharp and fully readable.

- The passport photo is less than six months old.

- There is no blur, glare, or cropping that cuts off any part of the document.

Blurred or unclear documents are automatically flagged and will be rejected, adding days to your approval timeline.

Verify Your Contact Information

Enter your active mobile phone number and a valid email address. You’ll be sent an OTP via SMS to verify your phone number, and a confirmation link by email to verify your email address. Both verifications must be completed before you can move on.

Create Account Security

Set a password of at least 10 characters, including a mix of uppercase letters, lowercase letters, numbers, and special characters — for example, something in the style of Napsa@1234. You’ll be asked to confirm the password by entering it a second time, so consider using a password manager to avoid mismatches.

Accept Terms and Conditions

Read through the data privacy consent and the terms and conditions carefully — these explain how NAPSA stores and uses your personal information. Once you’ve reviewed both, accept them to proceed, and submit your application for review.

Track Your Application

After submission, you’ll be given a reference number — write it down or save a screenshot, since you’ll need it to track your application. You’ll also receive SMS and email confirmation that your application has been received. Use the reference number on the portal to check your status while you wait for approval, which typically takes 2–3 business days.

After Approval

Once your profile is approved, you’ll receive confirmation by email and SMS, along with your NAPSA member number. From here, you can log in to your member dashboard, which gives you access to your contribution history, statements, and benefit information.

The most important next step is to complete your KYC (Know Your Customer) update — adding your bank account details and nominating beneficiaries. This is what NAPSA uses to process benefit payouts and withdrawals, so leaving it incomplete can significantly delay any future claim.

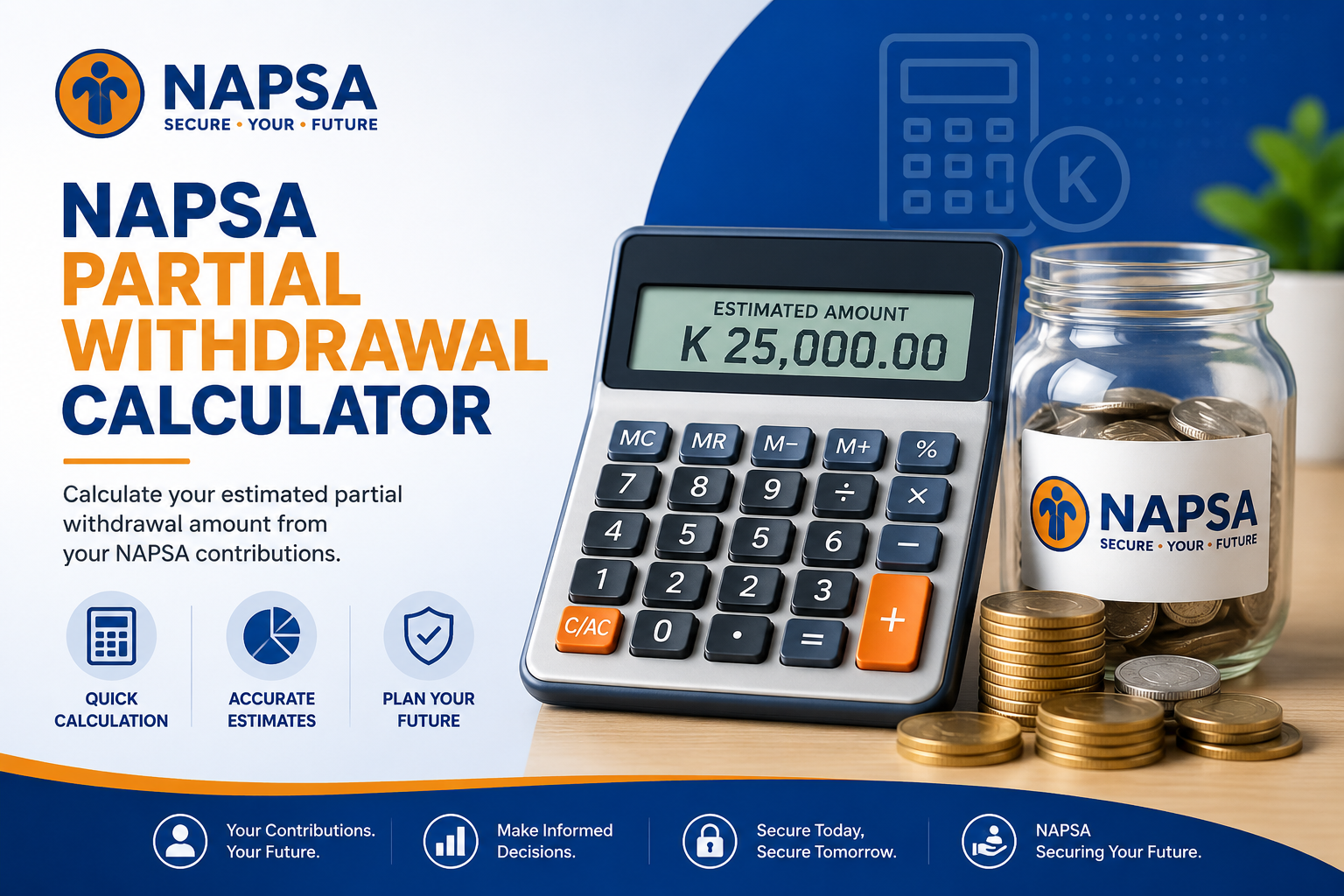

NAPSA Contribution Calculator (ZMW)

NAPSA contributions are calculated as a percentage of an employee’s gross monthly earnings, split between the employee and the employer, up to a statutory ceiling. Use the calculator below to estimate your monthly contribution in Zambian Kwacha based on your gross salary.

Estimate Your Monthly NAPSA Contribution

This calculator provides an estimate based on the standard NAPSA contribution structure (5% employee + 5% employer, applied to earnings up to the statutory ceiling). The ceiling is periodically revised by NAPSA — always confirm the current figure on the official NAPSA iCare portal or with your payroll provider before relying on this for payroll purposes.

Common Issues and Quick Fixes

| Issue | Solution |

|---|---|

| Document upload errors | Make sure files are under 5MB and in PDF, PNG, or JPG format |

| Phone verification fails | Confirm the number is registered in your own name with your network operator |

| Email verification problems | Check your spam folder and confirm the email hasn’t already been used for another NAPSA account |

| Application delays | Contact NAPSA support if there’s no response after 5 business days |

Frequently Asked Questions

How long does registration take?

Filling out the form typically takes 30–45 minutes if you have all your documents ready, with account approval taking an additional 2–3 business days.

Can I use the same email for multiple accounts?

No. Each email address must be unique and can only be linked to one NAPSA iCare registration.

What if my phone number is not registered in my name?

You’ll need a mobile number registered in your own name with your network operator, since OTP verification is sent to that number and tied to your identity.

Can foreign nationals register for NAPSA?

Yes. There are dedicated categories for foreign nationals working in Zambia and for those working outside Zambia under a NAPSA-linked arrangement.

What happens if I provide false information?

Providing false information can result in your application being rejected and may affect your ability to access benefits later, since your records are cross-checked against your submitted documents.

How do I track my application status?

Use the reference number provided after submission to check your application status directly on the iCare portal.

What file formats are accepted for document uploads?

PDF, PNG, and JPG files are accepted, with a maximum size of 5MB per document.

What’s Next?

Registration is just the first step. Once your profile is approved, here’s what most members and employers do next:

Update KYC Information

Add your bank details and nominate beneficiaries so payouts and claims can be processed without delay.

Register as Employer

If you run a business, register it with NAPSA so your employees can be enrolled and contributions tracked.

Submit Employee Returns

Upload monthly contribution returns for your staff through the employer portal.

Make Payments

Process monthly contribution payments directly through iCare’s payment options.

Related Resources

For payroll and compliance tasks related to NAPSA registration, these tools and guides may help:

2 Comments

This calculator guide is well structured, especially the eligibility and formula sections. For students, the same clarity is useful when choosing a calculator for exams: the question is not just whether a calculator works, but whether it is allowed and practical under test rules. I have been organizing exam calculator policy notes for that reason. Do you plan to add more education or exam-related calculator tools in the future?

Sure we very committed to update our site with fully structured Exam related calculator and more educated tools thanks.